Why Should You Diversify?

As 2019 approaches, and with US stocks outperforming non-US stocks in recent years, some investors have again turned their attention towards the role that global diversification plays in their portfolios.

For the five-year period ending October 31, 2018, the S&P 500 Index had an annualized return of 11.34% while the MSCI World ex USA Index returned 1.86%, and the MSCI Emerging Markets Index returned 0.78%. As US stocks have outperformed international and emerging markets stocks over the last several years, some investors might be reconsidering the benefits of investing outside the US.

While there are many reasons why a US-based investor may prefer a degree of home bias in their equity allocation, using return differences over a relatively short period as the sole input into this decision may result in missing opportunities that the global markets offer. While international and emerging markets stocks have delivered disappointing returns relative to the US over the last few years, it is important to remember that:

- Non-US stocks help provide valuable diversification benefits.

- Recent performance is not a reliable indicator of future returns.

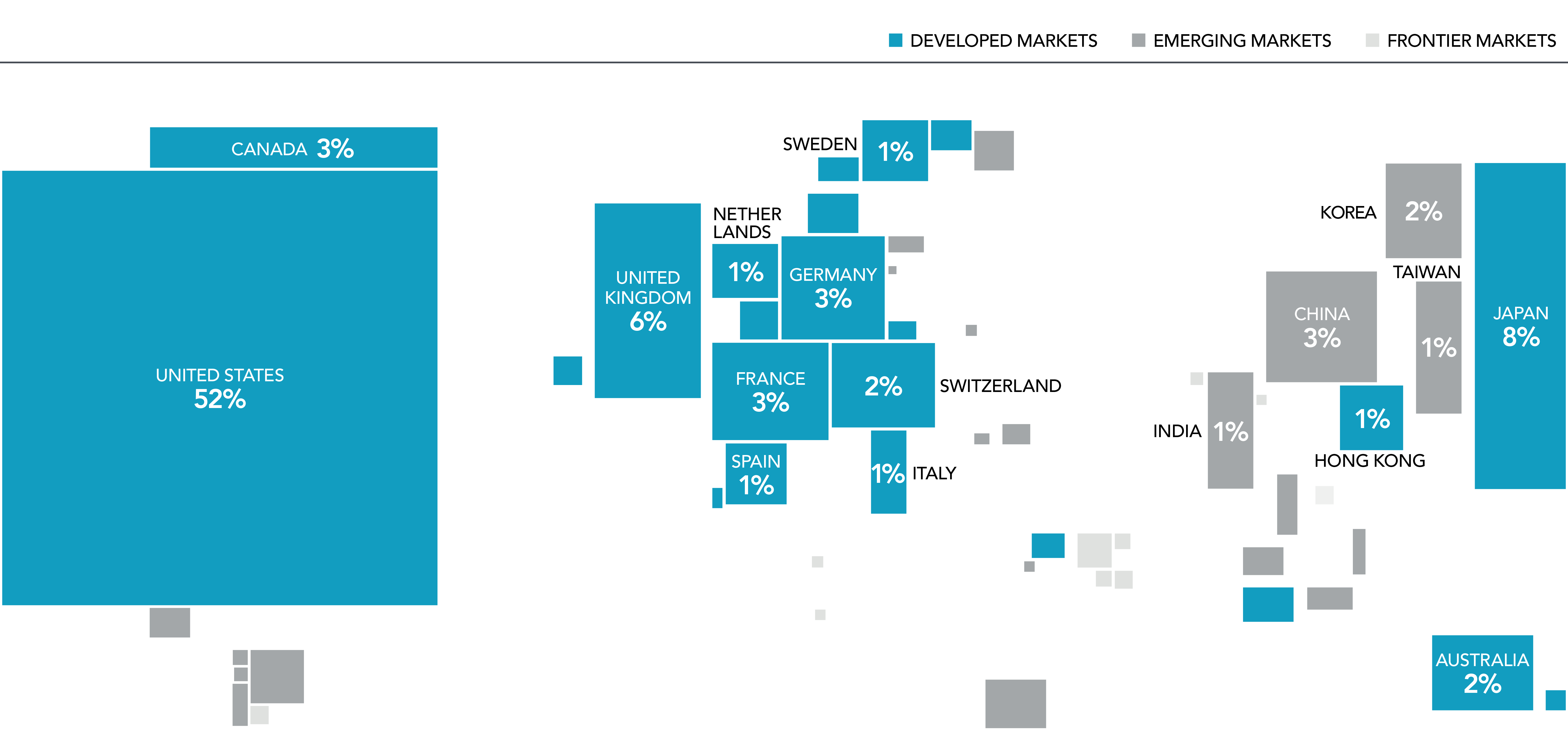

THERE’S A WORLD OF OPPORTUNITIES IN EQUITIES

The global equity market is large and represents a world of investment opportunities. As shown in Exhibit 1, nearly half of the investment opportunities in global equity markets lie outside the US. Non-US stocks, including developed and emerging markets, account for 48% of world market capitalization[1] and represent thousands of companies in countries all over the world. A portfolio investing solely within the US would not be exposed to the performance of those markets.

EXHIBIT 1. World Equity Market Capitalization [a]

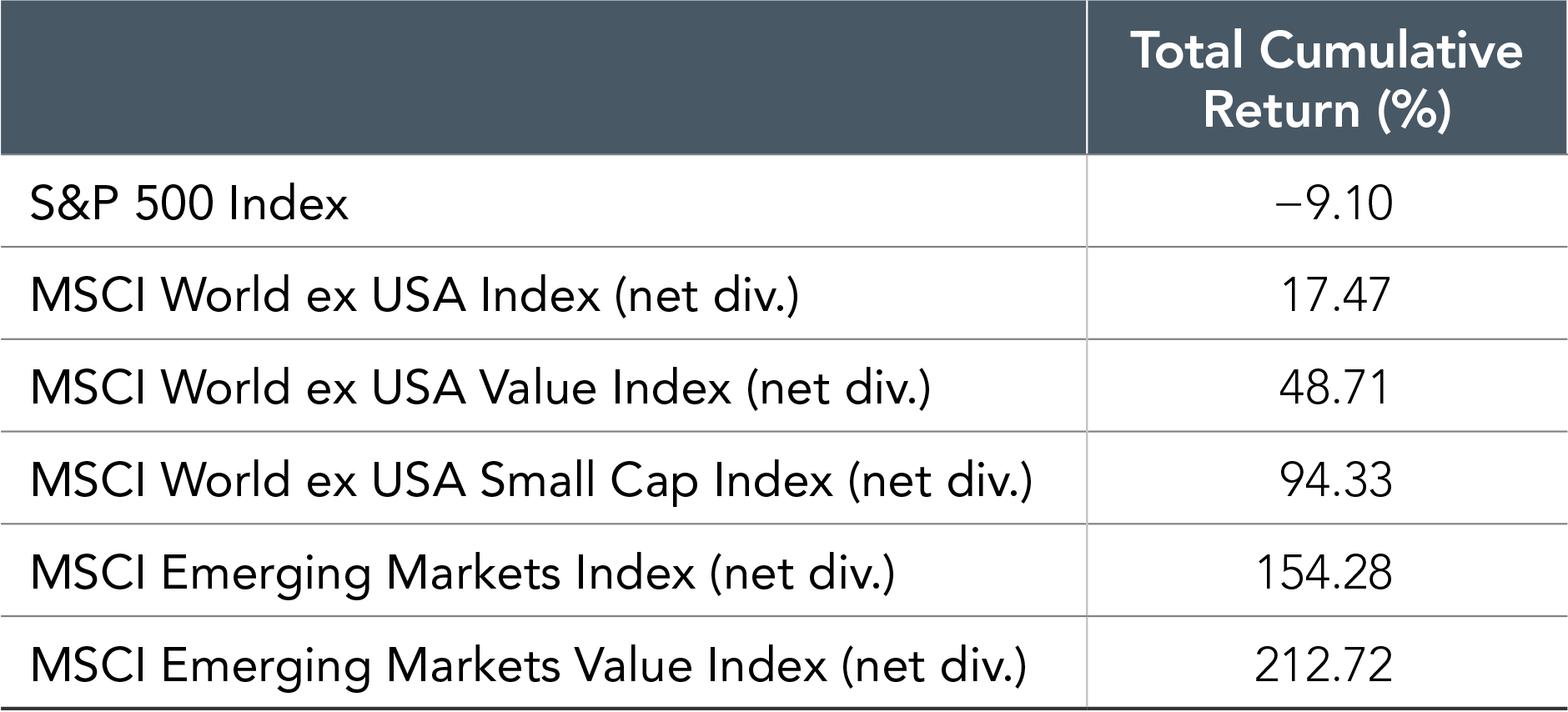

THE LOST DECADE

We can examine the potential opportunity cost associated with failing to diversify globally by reflecting on the period in global markets from 2000–2009. During this period, often called the “lost decade” by US investors, the S&P 500 Index recorded its worst ever 10-year performance with a total cumulative return of –9.1%. However, looking beyond US large cap equities, conditions were more favorable for global equity investors as most equity asset classes outside the US generated positive returns over the course of the decade. (See Exhibit 2.) Expanding beyond this period and looking at performance for each of the 11 decades starting in 1900 and ending in 2010, the US market outperformed the world market in five decades and underperformed in the other six.[1] This further reinforces why an investor pursuing the equity premium should consider a global allocation. By holding a globally diversified portfolio, investors are positioned to capture returns wherever they occur.

EXHIBIT 2. Global Index Returns, January 2000-December 2009

PICK A COUNTRY

Are there systematic ways to identify which countries will outperform others in advance? Exhibit 3 illustrates the randomness in country equity market rankings (from highest to lowest) for 22 different developed market countries over the past 20 years. This graphic conveys how difficult it would be to execute a strategy that relies on picking the best country and the resulting importance of diversification.

EXHIBIT 3. Equity Returns of Developed Markets [b]

In addition, concentrating a portfolio in any one country can expose investors to large variations in returns. The difference between the best- and worst‑performing countries can be significant. For example, since 1998, the average return of the best‑performing developed market country was approximately 44%, while the average return of the worst-performing country was approximately –16%. Diversification means an investor’s portfolio is unlikely to be the best or worst performing relative to any individual country, but diversification also provides a means to achieve a more consistent outcome and more importantly helps reduce and manage catastrophic losses that can be associated with investing in just a small number of stocks or a single country.

CONCLUSION

Over long periods of time, investors may benefit from consistent exposure in their portfolios to both US and non‑US equities. While both asset classes offer the potential to earn positive expected returns in the long run, they may perform quite differently over short periods. While the performance of different countries and asset classes will vary over time, there is no reliable evidence that this performance can be predicted in advance. An approach to equity investing that uses the global opportunity set available to investors can provide diversification benefits as well as potentially higher expected returns.

[1]. The total market value of a company’s outstanding shares, computed as prices times shares outstanding. [a]. As of December 31, 2017. Data provided by Bloomberg. Market cap data is free-float adjusted and meets minimum liquidity and listing requirements. China market capitalization excludes A-shares, which are generally only available to mainland China investors. For educational purposes; should not be used as investment advice. [2]. Source: Annual country index return data from the Dimson-Marsh-Staunton (DMS) Global Returns, provided by Morningstar, Inc. [b]. Source: MSCI country indices (net dividends) for each country listed. Does not include Israel, which MSCI classified as an emerging market prior to May 2010. MSCI data © MSCI 2018, all rights reserved. Past performance is no guarantee of future results. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated on an actual portfolio. Data Source: Dimensional Fund Advisors LP. Diversification does not eliminate the risk of market loss. There is no guarantee an investing strategy will be successful. Investment risks include loss of principal and fluctuating value. Sector-specific investments can also increase these risks. Environmental and social screens may limit investment opportunities. Small and micro cap securities are subject to greater volatility than those in other asset categories. All expressions of opinion are subject to change. This article is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services. Investors should talk to their financial advisor prior to making any investment decision.

Download PDF

![]()

wm = ic + ap + rm

wealth management investment consulting

advanced planning

relationship management

918-524-6325

4200 East Skelly Drive

Suite 350

Tulsa, OK 74135

info@everwealth.net

Wealth Management Advisors, LLC DBA Everwealth®, located in Tulsa, OK, is a Registered Investment Adviser under the Oklahoma Uniform Securities Act of 2004. We provide wealth management and financial planning services. Past performance is not necessarily indicative of future results. Investing involves risk, including the possibility of financial loss. Insurance-related business is offered through Riddle Financial Group, LLC, a separate company from Wealth Management Advisors, LLC DBA Everwealth. Please see our Disclosure section for important information.